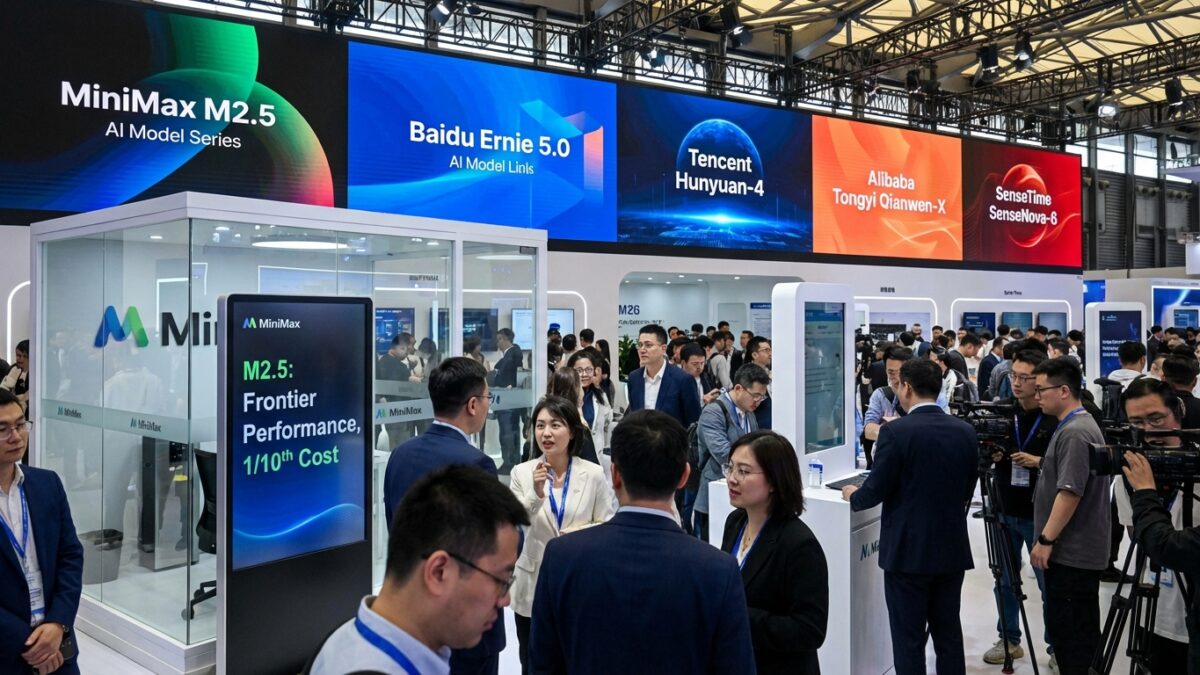

Five new artificial intelligence models were introduced in March 2026 by leading Chinese technology companies, including Tencent, Alibaba, Baidu, and ByteDance, in a concentrated demonstration of China’s rapidly advancing AI capabilities. The standout release, MiniMax’s M2.5 model, has drawn particular attention for reportedly rivaling the performance of top Western models while costing significantly less to run, intensifying the competitive pressure on companies like OpenAI, Anthropic, and Google. (Source: Mean CEO/AI News)

The MiniMax Breakthrough

MiniMax, a Chinese startup backed by Tencent, released its M2.5 model with capabilities that reviewers describe as competitive with Western frontier models at dramatically lower price points. The model’s release underscores a pattern that has been emerging since DeepSeek shook the AI industry in early 2025: Chinese labs are demonstrating that high-quality AI does not require the enormous budgets that American companies have been spending. (Source: Mean CEO/AI News)

The cost advantage is significant. While OpenAI’s GPT-5.2 and Anthropic’s Claude Opus models require expensive inference infrastructure, Chinese models like M2.5 are optimized for efficiency, running on less specialized hardware and offering API pricing that undercuts Western competitors by substantial margins. For developers and enterprises evaluating their AI stack, the economic argument for Chinese models is becoming increasingly compelling.

Open Source as Strategy

MIT Technology Review observed that Chinese AI firms’ near-unanimous embrace of open source has earned them significant goodwill in the global developer community and a long-term trust advantage. Unlike the largely proprietary approach of American AI companies, Chinese labs have released model weights and training methodologies that allow global developers to inspect, modify, and build upon their work. (Source: MIT Technology Review)

The strategic implications extend beyond developer relations. Open-source AI models cannot be easily controlled through export restrictions or sanctions. Once released, they propagate through the global developer ecosystem and become embedded in applications worldwide. MIT Technology Review predicted that in 2026, more Silicon Valley applications will quietly ship on top of Chinese open models, and the performance gap between Chinese releases and Western frontier models will continue shrinking from months to weeks, and sometimes less. (Source: MIT Technology Review)

The Frontier Model Landscape

As of March 2026, the frontier AI landscape includes several competing model families. OpenAI’s GPT-5.2 offers a 400,000-token context window. Anthropic’s Claude Opus 4.6 introduced effort controls that let developers tune intelligence, speed, and cost tradeoffs. Google’s Gemini 3.1 Pro offers significant free-tier access. xAI’s Grok 4.20, released February 17, implements a novel four-agent parallel processing architecture. DeepSeek V4 ships with native multimodal support. The sheer number of competitive options represents a dramatic change from the duopoly that ChatGPT and Gemini appeared to hold just two years ago. (Source: Mean CEO/AI News)

Enterprise Implications

For enterprises, the proliferation of competitive models creates both opportunity and complexity. Organizations can now evaluate a diverse range of providers across price points, capabilities, and deployment options. Coding-focused variants like GPT-5.3 Codex and Claude Code target developer workflows specifically, while medical and legal AI variants are being fine-tuned for specialized domains where they often outperform general-purpose models. (Source: Mean CEO/AI News)

AT&T’s chief data officer Andy Markus predicted that fine-tuned small language models will become a staple for mature enterprises in 2026, as cost and performance advantages drive adoption over generic large models. The Chinese competition reinforces this trend by demonstrating that smaller, more efficient models can achieve frontier-level results, challenging the assumption that only massive-scale American systems can compete at the top. The AI industry’s geographic monopoly is breaking down, and the implications for global technology competition, national security, and the pace of innovation are only beginning to be understood. (Source: TechCrunch)

Geopolitical Implications

The competitive dynamics between Chinese and Western AI development are being shaped by geopolitical forces as well as technical innovation. U.S. export restrictions on advanced AI chips to China have forced Chinese labs to develop more efficient architectures that achieve competitive performance with less powerful hardware. This constraint has paradoxically accelerated innovation in model efficiency, producing models that require less compute per token and can run on more widely available infrastructure.

For the global developer community, the availability of high-quality open-source Chinese models creates options that did not exist two years ago. Startups in developing countries that cannot afford API access to Western frontier models can now build competitive applications on locally hosted open-source alternatives. This democratization of AI capabilities has profound implications for global technology development and challenges the assumption that AI leadership will remain concentrated in a handful of American companies. The AI industry’s geographic monopoly is breaking, and the implications for technology competition, national security policy, and the pace of global innovation are only beginning to be understood. Samsung’s Galaxy S26 series at MWC Barcelona showcased on-device AI capabilities powered by these increasingly efficient models, demonstrating that the benefits extend directly to consumer products.

The enterprise implications extend further as organizations evaluate total cost of ownership. Chinese models on less specialized hardware offer not just lower API pricing but reduced infrastructure costs. For regulated industries requiring on-premises deployment, high-performance open-source models eliminate dependency on external providers. Specialized variants are emerging across industries: medical models trained on clinical data, legal models on case law, financial models on regulatory filings. Domain-specific models often outperform general-purpose systems within their specialties. The competitive intensity shows no signs of moderating, with OpenAI raising $110 billion, Anthropic pursuing massive funding, and Chinese labs iterating at speed. Enterprise customers must build flexible strategies leveraging the best models across a diverse landscape.